By SABRINA KARL

June 14, 2023

For people with cash savings in the bank, times are good. Rates on savings, money market, and certificates of deposit (CDs) are at their highest levels since at least 2007, with the best options offering you upwards of 5.00% APY. It’s an excellent time to make hay while the financial sun shines.

iStock image

But there are different ways to do that. And with the Federal Reserve perhaps still hiking the federal funds rate (the interest rate that influences savings and CD yields), choosing between savings vehicles with locked or variable interest rates will make a notable difference down the road.

Understanding Fixed vs. Variable Rates

Bank accounts in which you can deposit and withdraw at will, like savings, money market, and interest-paying checking accounts, virtually always have a variable rate. That means the bank or credit union can adjust the annual percentage yield (APY) it pays on your balance anytime it wants. And it doesn’t have to give you any advance warning.

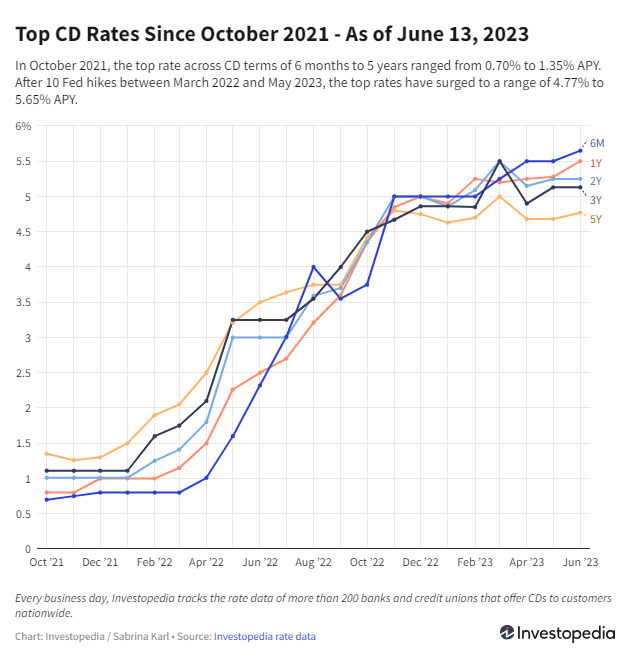

In contrast, you can put some of your cash savings into a CD at a bank or credit union. Here, the interest rate is fixed for the duration, or term, of the CD you choose to open. For instance, right now the best 1-year CD in the country is paying 5.50% APY. That means you are guaranteed to earn that rate for the full year you hold the CD, no matter what happens with Fed rate changes. This is true of any CD term, meaning opening a 5-year CD means you will be guaranteed the CD’s rate for a full five years.

The trade-off on CDs is that you must commit to keeping your funds there for the full term. If you opt to withdraw the funds before maturity, the bank or credit union will impose an early withdrawal penalty that will subtract from your interest earnings.

When a Fixed Rate Is Most Appealing

Opening a CD, particularly a mid- to long-term one, is especially savvy when you have funds you won’t need for a while and rates are high. That’s the situation we're in right now, with bank deposit rates sitting at 15-year highs due to the Federal Reserve’s aggressive rate-hike campaign that’s been underway since March 2022.

Because CD rates are at record levels, any CD you open now will lock in that stellar rate for months or years to come, no matter what the Fed does with the federal funds rate. Even after the Fed eventually begins to throttle back on rates—something that’s predicted will happen later this year or in 2024—your CD rate will be guaranteed until its maturity date.

In other words, you can use fixed rates to your advantage when rates are currently high but expected to decline in the not-too-distant future, enabling you to extend today’s great rates much further down the road.

When a Variable Rate Is Better

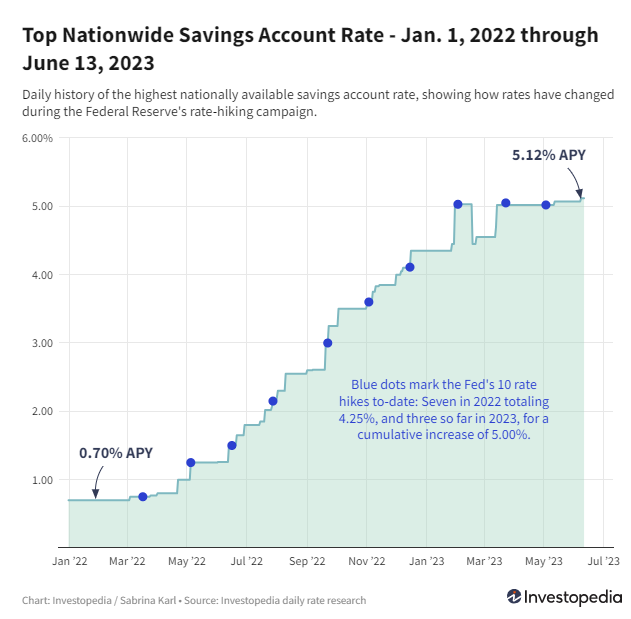

On the flip side, variable rates are a saver’s friend when interest rates are rising. That has been the case since the Fed began raising rates last year. Over the past 15 months, the Fed has implemented 10 rate hikes—many of them quite aggressive—to raise the federal funds rate by a cumulative 5.00%.1

As a result, the rates on high-yield savings and money market accounts have climbed throughout the Fed’s campaign. As you can see in the graphic below, the top-paying nationally available savings account was paying 0.70% APY before the Fed’s first rate increase. Since then, the top high-yield savings rate has surged to an eye-popping 5.12% APY today.

Anytime rates are expected to rise in the foreseeable future, variable-rate vehicles like savings and money market accounts are a great way to capture a high yield that will keep adjusting higher as rates increase.

So What Does That Mean Right Now?

The Federal Reserve’s rate-setting committee is meeting now, with a rate-decision announcement planned for Wednesday afternoon. It is overwhelmingly expected that the Fed will announce a rate pause this time, for the first time in 11 meetings. Today's report showing inflation continues to slow feeds that speculation even more.

But market watchers and traders who bet on where the federal funds rate is headed predict this is likely to be just a rate skip, not an end to the overarching campaign of raising rates. In fact, around two-thirds of interest rate traders currently forecast that the Fed will once again raise rates at its July 26 meeting.2

Since the Fed makes each rate decision based on the freshest economic indicators and financial news, predictions are just that, and can change at any time. But it’s a reasonable assumption that rates could rise a bit higher than they are now, though not likely by a large increment. That means we are probably at or very near the peak rate we’ll see in this Fed campaign.

As for where to put your savings, the variable rates of savings and money market accounts could still be winners for a bit longer, perhaps gaining even more ground. But once it appears the Fed is finished raising rates, yields on accounts with variable interest rates will plateau and start to decline, since banks often make rate decisions in advance of where they think the Fed rate is headed.

So we are perhaps approaching a tipping point on the near horizon, where locking in a fixed-rate CD while returns are at or near their peak is a smart move, before variable rates begin to drop on savings and money market accounts.

Rate Collection Methodology Disclosure

Every business day, Investopedia tracks the rate data of more than 200 banks and credit unions that offer money market, savings accounts, and CDs to customers nationwide, and determines daily rankings of the top-paying accounts. To qualify for our lists, the institution must be federally insured (FDIC for banks, NCUA for credit unions), and the account's minimum initial deposit must not exceed $25,000.

Banks must be available in at least 40 states. And while some credit unions require you to donate to a specific charity or association to become a member if you don't meet other eligibility criteria (e.g., you don't live in a certain area or work in a certain kind of job), we exclude credit unions whose donation requirement is $40 or more.

ARTICLE SOURCES

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in our editorial policy.

- Federal Reserve Board. Open Market Operations.

- CME Group. CME FedWatch Tool: https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

Eugene Yashin, MBA, CFA®

Matthew Etter, CFP®

Steve Tuttle, MBA