By DAWN PAPANDREA

May 2, 2023

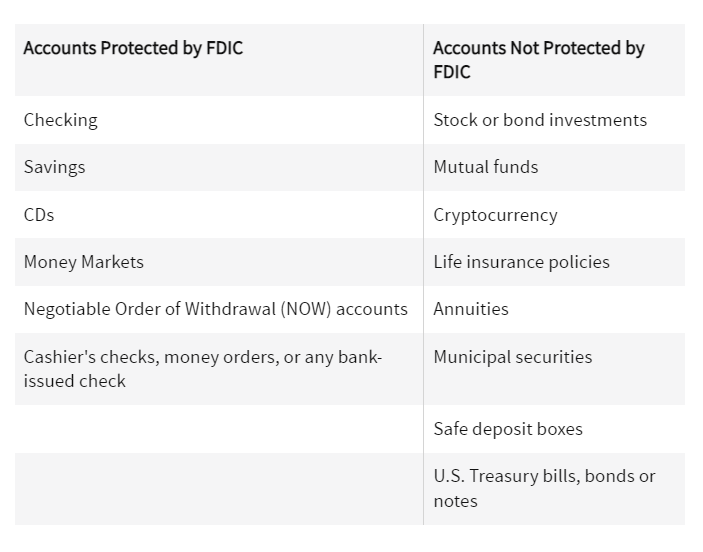

When your bank fails, the first thing to keep in mind is that you won’t lose all your deposits. The Federal Deposit Insurance Corporation (FDIC) insures bank accounts up to $250,000 per depositor, per account category.1 So, unless your bank is not insured by the FDIC or you have deposited more than the FDIC limit, your money is safe if your bank fails.

The FDIC will notify you in the case of a bank failure like the Silicon Valley Bank and Signature Bank closures in March 2023. Your insured deposits will either be moved to another FDIC-insured bank or paid out to you. Learn more about why banks fail, how FDIC insurance works to help you recoup your money, and how to protect your finances.

iStock image

KEY TAKEAWAYS

- In most cases, a bank failure is the result of owing more to creditors and depositors than what their assets are worth.

- If your bank fails, up to $250,000 of deposited money (per person, per account ownership type) is protected by the FDIC.

- When banks fail, the most common outcome is that another bank takes over the assets and your accounts are simply transferred over. If not, the FDIC will pay you out.

- Funds beyond the protected amount may still be reimbursed, but the FDIC does not guarantee this.

Why Do Banks Fail?

Banks typically fail when they become insolvent, or when the value of their assets drop to levels below what they owe to creditors and depositors.

Banks do not keep all of the cash that is deposited sitting in a vault. Instead, those funds are lent out to other customers or used to make investments. Banks can become insolvent, for example, if they make risky investments and market conditions cause them to lose money, or they lend to people or businesses that don’t meet their obligations.

Note: When customers become aware of a bank’s financial stress, they may rush to withdraw their money out of fear the bank will fail. This is called a bank run. When too many depositors clear their accounts at once, that can actually cause the bank to fail.

What Happens If My Bank Fails?

Once a bank can no longer afford to make good on its obligations to customers and creditors, the FDIC steps in. Here’s what typically happens.

- The FDIC announces that the bank is closed, and the FDIC is appointed as its receiver so it can help use the bank’s assets to pay depositors and creditors.

- In most cases, the FDIC will try to find another banking institution to acquire the failed bank. If that happens, customers’ accounts will simply transfer over to the new bank. You will get information about the transition, and you will likely get new debit cards and checks (if applicable).

- If another bank doesn’t take over the assets, the FDIC will send depositors a reimbursement check “as soon as possible.”

- The FDIC is not obligated to return funds beyond the $250,000 that is insured, but you still have some recourse if you’ve had more than that in an account category. First, you can request a receiver's certificate, which lets you claim your funds when the bank's assets are liquidated.2

TIP: The best way to avoid losing money if your bank fails is to not exceed the $250,000 FDIC-insured limit. If you have more than that, you can either open an account in another bank, or open an account in the same bank but with a different ownership category (more on ownership categories in the table below).

Examples of Bank Failures

Bank failures are a lot less common since the FDIC started operation in 1934. Before that, thousands of banks failed during the Great Depression—4,000 in 1933 alone.3 But bank failures still occur. In some cases, broader market trends can trigger bank failures, such as when 25 banks failed in 2008 amid the housing crisis.4 Banks can fail for other reasons as well, such as internal mismanagement.

Let’s look at some notable bank failures:

- Silicon Valley Bank and Signature Bank: In what was called the first social media bank run by many news outlets, Silicon Valley Bank and Signature Bank abruptly closed in 2023. News of their financial troubles spread on platforms like Twitter, causing customers to panic and pull their money.

- The largest bank failure: Washington Mutual (WaMu) is the largest bank failure in terms of assets. The bank collapsed during the 2008 financial crisis at a time when it had $307 billion in assets. JPMorgan Chase took over WaMu.5

- The last big in-person bank run: In 1984, Continental Illinois National Bank and Trust Company was one of the largest U.S. banks when it found itself in financial trouble. When rumors began to spread, there was a run on deposits at the bank’s branches. Depositors withdrew $10.8 billion.6

565

The number of banks that have failed since 2000, as of April 10, 2023. The FDIC's Failed Bank List includes details on them.7

Do You Lose Any Money If Your Bank Closes?

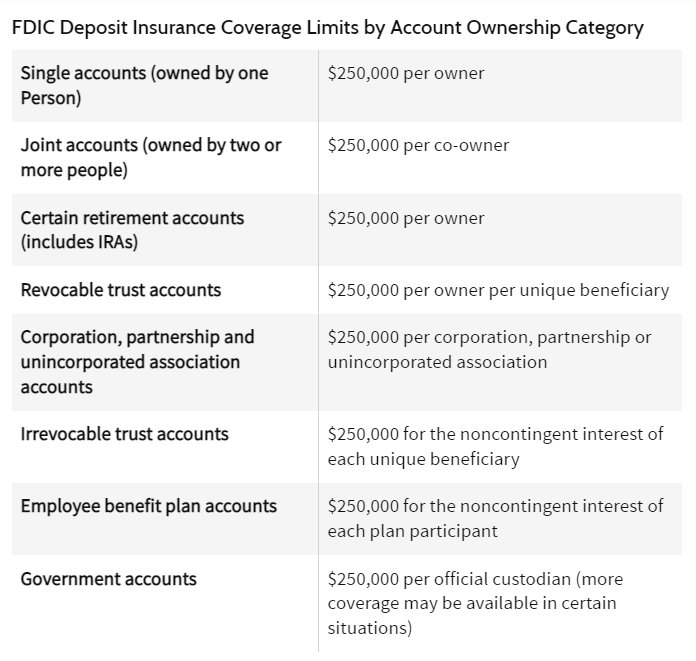

If your deposits are under the FDIC insurance limits ($250,000 per depositor per ownership type), then you won’t lose any money if your bank closes. But it’s important to understand what types of accounts are insured and what the limit means.

You also need to pay attention to ownership categories.

If you have bank accounts with credit unions, those funds are protected by the National Credit Union Administration (NCUA), which federally insures credit unions.8

What if You Have Multiple Accounts?

If you have multiple accounts at one bank, such as an individual checking account and savings account in the same bank with a total of $300,000, FDIC insurance won’t fully protect you. It only insures up to $250,000 per depositor, per account ownership type. You could lose $50,000 because, in this case, the accounts are in the same ownership category.

However, if you had a joint checking account with your spouse and your own savings account, FDIC insurance would fully protect you because joint accounts and individual accounts are two different ownership categories.

Even if you had more than the $250,000 limit deposited, you might not lose any of your funds. If another bank takes over, your money will simply transfer there. If not, the federal government may cover the remainder of your funds, as it offered to do after the Signature and Silicon Valley Bank failures. Ultimately, all customer assets were protected when Flagstar Bank took over Signature Bank and First Citizens Bank & Trust Company took over Silicon Valley Bank.

Who Takes Over a Failed Bank?

When a bank fails, another bank will commonly take over the assets. When this happens, depositors and/or borrowers of the failed bank will automatically become customers of the new bank. If the FDIC doesn’t find another bank to take over, it will send out checks for the insured deposit amounts, typically within a few days.2

When a Bank Fails, Where Does Insured Money Come From?

The FDIC maintains the Deposit Insurance Fund (DIF), which it can draw from if it needs to pay out insured balances if a bank fails. That fund is also used to help resolve failed banks. The DIF is funded by insurance premiums that banks pay called assessments, as well as from interest earned on investments in U.S. government obligations.9

What Happens to My Direct Deposits If My Bank Closes?

What happens to your direct deposits when your bank fails depends on the fate of the failed bank. If another bank takes over, your direct deposits will automatically redirect to the new bank. If there is no acquiring bank, then the FDIC will try to find an institution to temporarily handle direct deposits, mainly so Social Security recipients do not experience any delays. Impacted customers will be updated about any changes to their direct deposits.2

What Happens to Checks and Automatic Payments That Have Not Cleared an Account Before My Bank Is Closed?

If your bank fails and you have checks that didn’t clear or automatic payments set up, you will be responsible for working with your creditors and lenders to make alternate payment arrangements. Your originally scheduled payment will be returned unpaid with a notation that your bank is closed. However, this will not impact your credit as long as you set up an alternate payment method.2

Can I Access My Safe Deposit Box If My Bank Closes?

Safe deposit boxes are physically kept in a bank branch, and you can usually retrieve the contents the day after the bank closure. If another bank acquires your bank, your branch should reopen the next business day, and you can remove your items at that time. Otherwise, the FDIC will send you a letter with instructions for how to get your items.2

The Bottom Line

Though bank failures get a lot of media attention, customer’s finances are usually not severely impacted. As long as you do business with an FDIC-insured institution and keep less than $250,000 per account ownership category, your funds will be safe if your bank fails. Although, you might face some minor inconveniences like waiting for a new debit card or updating your automatic payments.

Article Sources:

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in our editorial policy.

- Federal Deposit Insurance Corporation. "Deposit Insurance FAQs."

- Federal Deposit Insurance Corporation. “When a Bank Fails - Facts for Depositors, Creditors, and Borrowers.”

- Federal Deposit Insurance Corporation. “Historical Timeline.”

- Federal Deposit Insurance Corporation. “Bank Failures in Brief – 2008.”

- Federal Deposit Insurance Corporation. “JPMorgan Chase Acquires Banking Operations of Washington Mutual.”

- Federal Reserve History. “Failure of Continental Illinois.”

- Federal Deposit Insurance Corporation. "Failed Bank List."

- National Credit Union Administration. "Share Insurance Fund Overview."

- Federal Deposit Insurance Corporation. “Deposit Insurance Fund.”

Eugene Yashin, MBA, CFA®

Matthew Etter, CFP®

Steve Tuttle, MBA