By Katie Oelker

Jan. 4, 2023

The new year is here, and it's time to start thinking about filing your taxes. Changes were made to many tax credits and deductions in 2022 that experts say could lead many people to owe money when they file their IRS returns in 2023.

This is the first year since the pandemic when financial relief has slowed down, so many tax credits and deductions are reverting back to where they were in years prior. But there are also shifts in the standard deduction amounts and income tax brackets, which happen annually.

iStock image

- With pandemic relief programs expiring, you could see a smaller tax refund this year.

- Several temporarily boosted tax credits, including the popular child tax credit, have reverted to prior levels.

- The standard deductions and income tax brackets have also shifted due to inflation.

Here are six of the most important changes to be aware of before you file your 2022 return.

1. Standard deductions are larger

A standard deduction is a specific amount that you can subtract from your income, and it's adjusted each year for inflation. How much you get is based on a few factors: your filing status, your age, and if someone else can claim you as a dependent.

"The standard deduction's increase for inflation means fewer Americans are likely to claim itemized deductions," says Sean Mullaney, a financial planner and accountant with Mullaney Financial & Tax, Inc. "For those claiming the standard deduction, their refund will increase or the amount due will decrease because of this change."

For 2022, the standard deduction increased $800 to $25,900 for married couples filing jointly. For single taxpayers it increased $400 to $12,950. And for people using the head of household filing status (i.e. single parents), the standard deduction increased to $19,400, up $600 from 2021.

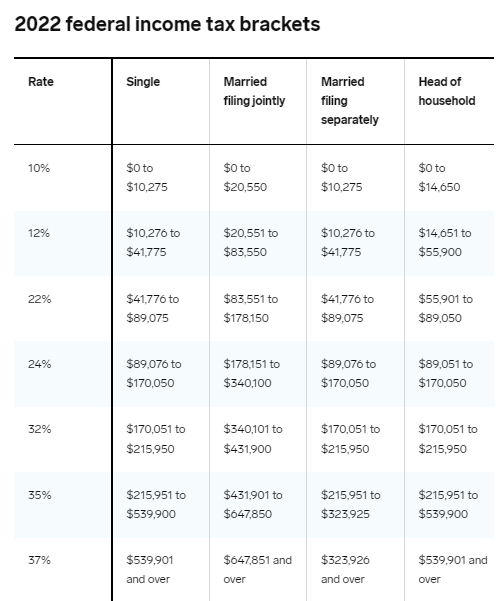

2. Income tax brackets shift

Tax brackets have gone up for 2022, but the tax rates stay the same.

"This means that more of your money is taxed at lower rates as opposed to the year before," says Logan Allec, an accountant and owner of Choice Tax Relief. "If your income tracked about the same as the tax brackets' income ranges shifted by, it may be a wash for you."

Adds Mullaney: "Those whose income and tax withholding stayed constant should generally expect to see an increased tax refund or reduction in the amount due."

3. The child tax credit is smaller

With most of the pandemic relief programs now behind us, some tax credits, including the child tax credit (CTC), will shrink for many families.

For the CTC, the credit amount will drop to a maximum of $2,000 per dependent under age 17 for 2022, down from $3,600 for children under age six or $3,000 for children under age 18 in 2021.

"This will cause many parents and others with dependents who are minors to see a refund decrease from last year," Allec says. Additionally, taxpayers once again need to have at least $2,500 in earned income to qualify for the refundable portion of the credit (in 2021, the income floor was temporarily suspended).

Note: The recovery rebate credit, which you could use over the past two years to claim any missing stimulus checks during tax time, is no longer available on Form 1040.

4. Income thresholds drop for the child and dependent care credit

Another tax credit change to note is that the temporary expansion of the child and dependent care credit expired. This credit helps parents who pay out of pocket for childcare expenses that enable them to work to claim a credit that's equal to 20% to 35% of those total expenses. Taxpayers with higher incomes can claim the smaller credit.

For qualifying taxpayers earning up to $125,000 in 2021, the maximum credit was substantially more generous and potentially refundable (up to $4,000 for one qualifying person and $8,000 for two or more qualifying persons). For 2022, only those earning $15,000 or less can qualify for the maximum credit, which has shrunk to $1,050 for one qualifying person and $2,100 for two or more qualifying persons. It's also no longer refundable.

5. Earned income tax credit shrinks for childless taxpayers

The earned income tax credit (EITC) was temporarily expanded in 2021 to help moderate and low-income workers without children get a bigger tax break, but that relief has ended.

For the 2022 tax year, single filers with no children who earn less than $16,480 can get a maximum credit of $560, down from $1,502 in 2021.

Quick tip: You can check if you qualify for the child tax credit, child and dependent care credit, or earned income tax credit by entering your income and dependent information on the IRS website.

6. No more $300 charitable deduction

During the pandemic, the IRS allowed taxpayers to reduce their gross income by up to $300 (or $600 if married and filing jointly) if they donated in cash to tax-qualified charities. That so-called above-the-line deduction is no longer available. Instead, individuals who want to write off their charitable donations must itemize their deductions.

As Allec points out, "A $300 deduction at the 24% marginal tax rate really only results in a $72 decrease in tax, so losing that deduction won't really make much of a hit for many taxpayers."

Putting it all together

So what does all this mean for your tax return? Allec says that in general, these changes "mean more people will wind up owing or getting a smaller refund than they did the past couple years."

That's because the size of several tax credits and deductions, and the eligibility requirements, have gone back to pre-2021 levels, primarily targeting moderate- and low-income workers rather than large swaths of the US population.

Be sure to gather all the necessary income documentation, take your time filling out your tax forms, and hire an accountant if needed. Filing taxes can be stressful, but being prepared can help it go as smoothly as possible.

Subscribe to Business Insider's Financial Insights Newsletter

This Business Insider article was legally licensed by AdvisorStream

Eugene Yashin, MBA, CFA®

Matthew Etter, CFP®

Steve Tuttle, MBA